In the current interest cycle in the American market, will we find investment to be a danger or an opportunity? In this article, we will explore the current complex economic landscape, focusing on the debate over the possibility of a “soft landing” amid the Federal Reserve’s aggressive cycle of interest rate hikes. We’ll look at how factors like the U.S. economy, consumer behavior, interest costs, and inflation intertwine to shape your financial future. Additionally, we will offer insights into how investors can make informed decisions to protect their wealth in times of uncertainty. From financial investments to investments in education, health and relationships, we will explore strategies to face economic challenges with confidence.

We are in the midst of the second most aggressive cycle of interest rate increases in the Federal Reserve’s history, and we expect to see a soft landing. However, almost every Federal rate hike cycle in the past has resulted in a hard landing, i.e., a recession.

The combination of declining economies, restarting student loan payments and rising interest and fuel costs are poised to affect consumer spending, which represents the biggest driver of the U.S. economy.

With markets appearing to underestimate the risk of a hard landing, you may want to act cautiously in your portfolio by reducing risk, avoiding leverage, keeping cash on hand, investing in gold and long-term government bonds, and adjusting your equity exposure to defensive sectors.

A summer of slowing inflation, plentiful job opportunities and solid consumer spending have raised investor hopes that the U.S. economy can achieve something truly rare: the longed-for soft landing. However, history and the current scenario suggest that investors are likely overly complacent, just as they have been before every US recession over the past 40 years. Here’s why a hard landing is still the most likely scenario and how you can prepare your wallet to weather the impact.

What is the difference between a hard landing, a soft landing, and no landing at all?

When the economy becomes excessively heated, it can lead to a potentially damaging rise in inflation. To combat this situation, the Federal Reserve (the Fed) generally chooses to increase interest rates, a measure that tends to cool economic activity and stabilize prices. The Fed’s goal is to achieve a soft landing: that ideal scenario in which the economy weakens enough to contain inflation but remains strong enough to avoid a recession. However, with each rate hike cycle, there is also the risk of a hard landing, in which the impact of these rate hikes actually drives the economy into a recession. Furthermore, there is the risk of a no-landing scenario, in which inflation remains high and the economy is not affected by rate increases. Currently, this last scenario does not appear to be in the cards, as we are already witnessing evidence of a slowdown in growth and inflation.

How challenging is it to achieve a soft landing?

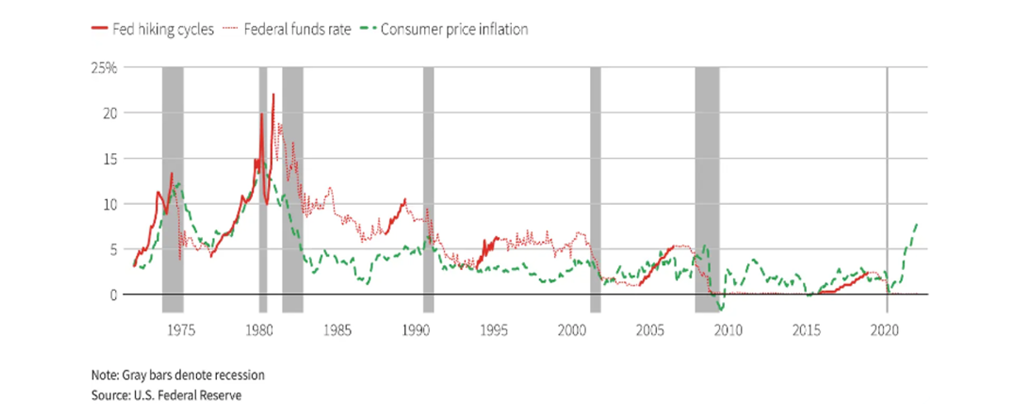

Well, that’s the point, but the Federal Reserve’s (Fed) track record has been mixed at best. The chart below presents each of the Fed’s interest rate increase cycles since the 1970s (solid red line), US inflation (dotted green line), and recessions (shaded gray bars). In most cases, aggressive interest rate increases have been followed, sometimes very quickly, by a recession. The only clear example of a successful soft landing was in the mid-1990s, when the central bank raised interest rates from 3% to 6% without causing the economy to collapse.

Given the current widespread debate over whether the Federal Reserve’s continued monetary tightening will tip the economy into a recession, it is critical to keep in mind the magnitude of the current rate hike cycle: it is the second most aggressive in the Federal Reserve’s 110-year history. In other words, except for a cycle of rate hikes in the 1980s, all other rate hikes have been less severe than the current one, and most of them have resulted in recessions. Therefore, if we look at history as a guide, the likelihood of the Fed smoothing this transition is low.

However, this has not stopped many investors and economists from being overly optimistic about how events will unfold. Perhaps this is because they often assume that what will happen in the economy will be some kind of extension of what happened previously. However, this linear forecasting method is not effective when it comes to non-linear events such as recessions.

In October 2007, just two months before the start of the Great Recession, then-San Francisco Federal Reserve President Janet Yellen declared that “the most likely outcome is that the economy continues toward a soft landing.” She was far from the only optimist.

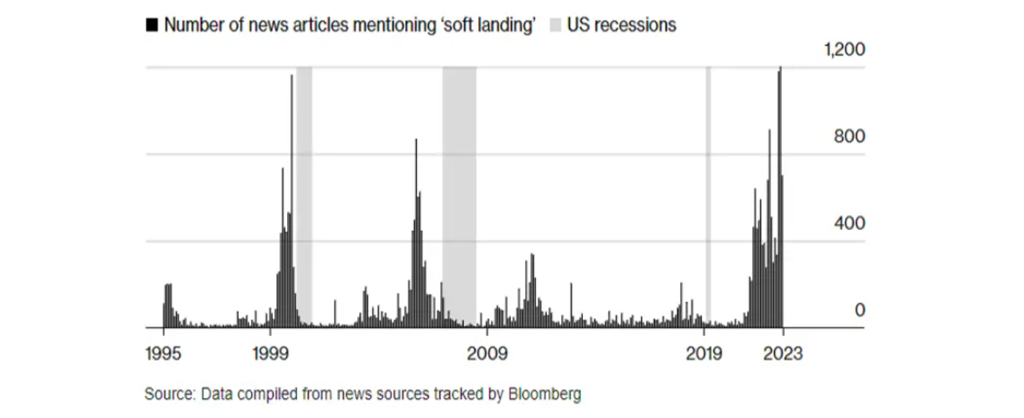

In fact, to illustrate how often people’s predictions are wrong, consider this chart that shows that expectations of a soft landing often peak before the actual hard landings occur.

Can the American consumers save the day?

Central to the case for a soft landing is the fact that consumer spending, which accounts for about two-thirds of the U.S. economy, has remained remarkably robust. Even with uncontrolled inflation, the country’s spending has not decreased (at least, not yet).

During the pandemic, many Americans have managed to save, saving stimulus checks and government benefits while cutting back on spending on luxuries like dining out and vacations. These savings created a kind of financial cushion that helped weather rising prices without significantly reducing spending, which in turn protected the economy from a recession. However, this money was destined to run out. According to the Federal Reserve’s most recent study of household finances, all but the richest 20% of Americans have spent those savings and now have less money than they did at the start of the pandemic.

This puts households in the United States in a dilemma: spend less or resort to borrowing to maintain their lifestyles. However, with the Fed’s interest rate hikes making credit more expensive and harder to access, Americans will likely have to reduce their spending. To put this situation into perspective, consider this: Interest payments now consume 2.5% of Americans’ disposable income, or the money left over after paying taxes. This is the highest percentage since September 2008.

Additionally, rising oil prices are forcing consumers to spend a greater portion of their disposable income on gasoline. Combined, interest and gasoline spending accounted for 4.7% of disposable income in the United States last month, the highest percentage since August 2014. Increases in the proportion of income going to interest payments or gasoline expenses often precede recessions, and this recent increase in both poses a double threat to the economy as it reduces Americans’ discretionary income, the money left over after paying taxes and essential expenses such as housing, food, interest, gas and utilities. Lower discretionary income, in turn, decreases consumer spending.

What’s more, all of this happens just as student debt payments are about to resume after a long break. These monthly payments were suspended more than three years ago during the height of the Covid crisis, but that relief ends this month. Therefore, millions of Americans will once again be saddled with an average of $200 to $300 in monthly debt expenses.

What does all this mean?

The conjunction of declining economies, the return of student loan payments, and rising interest and gasoline costs will have a significant impact on consumer spending, which, let’s not forget, is the engine of the United States economy. We’re already seeing this impact: Consumer spending rose just 0.1% in August, after adjusting for inflation, marking the weakest reading since March.

However, markets appear to be underestimating the risk of a hard landing. This implies that a slowdown could surprise many people and trigger a series of impulsive adjustments. Given this risk, it may be advisable to take a cautious approach to your investments. This includes reducing risk exposure and ensuring your portfolio is adequately diversified and free from leverage. It may also be wise to reduce equity exposure or consider greater positioning in quality companies in defensive sectors such as consumer staples and healthcare. When it comes to fixed investments, replacing high-yield corporate bonds with investment-grade bonds or long-term government bonds can be an effective strategy, as these assets can do well during a recession. Including a gold reserve and reducing exposure to other commodities, especially industrial metals such as copper and aluminum, and energy, may also be measures to consider.

Finally, it may be wise to keep some cash on hand, possibly through money market funds, which are currently offering yields in excess of 5%. We discuss the key roles that cash can play in a portfolio and analyze these funds in detail here. Remember that in times of economic uncertainty, having liquidity on hand can provide a valuable safety net to protect your wealth. Stay informed about market conditions and be prepared to adjust your investment strategy as needed to protect your financial assets.

Also, remember that diversification is essential. Avoid concentrating all your investments in a single asset class or sector of the economy. Instead, spread your investments across different asset classes and sectors to reduce risk.

In the current climate, it is crucial to remain well informed and adapt your investment strategy as the economic scenario evolves. Keep up with economic, political and global news that could impact financial markets and consider consulting a financial advisor for personalized guidance based on your specific financial situation.

Remember that investing always involves risks, and it is essential to be prepared for market fluctuations. Maintaining a cautious mindset and making informed investment decisions are essential steps to protecting your wealth during periods of economic uncertainty.

If you are considering making new investments or reviewing your financial strategy, it may be useful to explore some additional options that can help protect your assets in uncertain times. There are many free online resources, courses and books that can help you better understand financial markets and make informed decisions.

01) Investments in Health and Wellbeing

Remember that your physical and mental well-being is also an important investment. Invest in healthy habits, regular physical activity and health care to ensure your long-term quality of life.

02) Investments in Professional Skills

If possible, invest in professional development. Acquiring new skills and knowledge can increase your employment opportunities or open doors to new careers, providing long-term financial security.

03) Emergency Reserve

Keep an emergency fund equivalent to at least three to six months of expenses. This reserve provides a financial cushion in case of unexpected medical expenses, job loss or other financial emergencies.

04) Investments in Technology

In a digital world, staying up to date with technology is crucial. Investing in secure devices, antivirus software, and learning about online security practices can protect your personal and financial information.

05) Investments in Relationships

Don’t underestimate the power of a solid support network. Healthy relationships and social support can provide emotional support and, in some situations, financial assistance in times of need.

06) Investments in Sustainability

Consider sustainable practices in your lifestyle, such as saving energy at home, reducing plastic consumption, or supporting eco-friendly companies and initiatives. In addition to contributing to the environment, these choices can often save you money in the long run.

Remember that diversification doesn’t just apply to financial investments, but also to your lifestyle and the choices you make to ensure your long-term security and well-being. If you are contemplating on kickstarting forex and CFDs trading to diversify your investment portfolio, the ZERO Markets team is there to guide you through every step of the way, with trust, transparency, and full disclosure on the risks of Contract for Differences trading. Head over to our FAQ & Support page, or simply get on a live chat with us now and start trading with the best team behind you: the ZERO Markets team.

ZERO Markets is a trusted broker offering CFD trading in the global market. ZERO Markets is fully regulated and licensed for your comfort and security. We offer the best trading environment with reduced spreads from 0.0 pip, latest technology platforms and instant deposit channels.

Trade Responsibly: This e-mail may contain general advice which does not take into account your individual circumstances or objectives. CFD derivative products are highly leveraged, carry a high level of risk and are not suitable for all investors. Features of our products including fees and charges are outlined in the relevant legal documents available on our website. The legal documents should be considered before entering into transactions with us. ZERO Markets does not accept applications from residents of countries or jurisdictions where such distribution or use would be contrary to local laws or regulations. Clients receiving services in Saint Vincent and the Grenadines: Zero Markets LLC, which is a registered company of St. Vincent and the Grenadines, Limited Liability Number 503 LLC 2020 uses the Domain www.zeromarkets.com. Please refer to our SVG Privacy Policy. If you are not the intended recipient of this email please do not print, copy or distribute its content or attachments.

Leave a Reply